“Market cap is a silly made up number and always has been. Only the price you can sell at matters.”

–Richard Heart (HEX Founder)

Foreword

Before getting started, I’d like to thank the HEX community for helping Nomics.com understand HEX a bit better. In particular, I want to thank Dev Kyle and Gunther (creator of HEX Audit) for lending their time to help my co-founder and I understand HEX’s supply. We’ve learned a lot on this journey, and come away impressed with the strength and quality of the HEX community.

I also want to apologize: we got HEX’s circulating supply wrong, and now need to make an adjustment that lowers HEX’s market cap. I wish we’d had a better understanding of HEX two years ago when we first listed your asset. I’d much rather (1) not have to make any adjustments, or (2) have to make corrections that increase your market cap.

I was originally going to title this blog post “Hex: Decentralized Infrastructure, Centralized Ownership, Circulating Supply & Market Cap” but that was too wordy.

I have two asks:

- If you have comments, questions, or criticisms about this post, I ask that you keep them to the comments section. There’s only one of me and hundreds of folks on Twitter and I (unfortunately) do not have the bandwidth to monitor every question on every thread and sub-thread there. Especially when I’m sometimes tagged, and sometimes not, or Nomics is tagged. Post away on Twitter if you want, but I’ll be monitoring comments here.

- Please give me time to respond. The last time I engaged in a significant way with the HEX community, more responses led to more impatience from the community. I’d be on vacation with my wife, or putting my kids to bed, and folks would be upset when I didn’t respond to a question within 20 minutes.

There’s a lot of ground to cover here, so I’m going to structure this as an FAQ.

I should disclose that I’m a HEX holder (although I don’t identify as a HEXican) and that I participated in the PulseChain sacrifice. We’ve experienced a lot of support from the HEX community, and for this we’re grateful. That said, we need to make some changes to the HEX supply.

If you dislike this article, our stance, me, or Nomics I am sorry. I’ve been grateful for your patronage of Nomics to date and we’ll understand if you now want to go to another aggregator that gives HEX a higher rank. After lots of engaging on Twitter, and conversations with core members of the HEX community, I believe we’ve done more to try and understand HEX than any of our competitors. And I hope we get some credit for that (i.e. compare our level of interactiveness and responsiveness to that of CMC or CG).

I can promise you this…

- We’ll never copout by gatekeeping you at 201 market cap ranking (like CoinMarketCap) or failing to post a circulating supply at all (like CoinGecko).

- We’ll do our very best to list your PulseChain assets before anyone else. We’ll try and list every single PulseChain asset, even very new ones with low volumes.

- We’ll always stay in dialogue with you and we’re open to evolving the stance outlined below over time.

How to Have A #1 Market Cap Asset In Less Than An Hour (If You Read Nothing Else, Please Read This)

This is what happens when Coins x Price = Market Cap…https://t.co/LBz2s4hWXa

How Rank #1 in Marketcap in 1 Hour

1: Mint 100 Trillion BEP-20 Tokens on BSC

2: Give all but 100 to yourself

3: Put the remaining 100 on PancakeSwap against 0.1BNB and then buy 1 token— clay.c/ (@ClayCollins) November 8, 2021

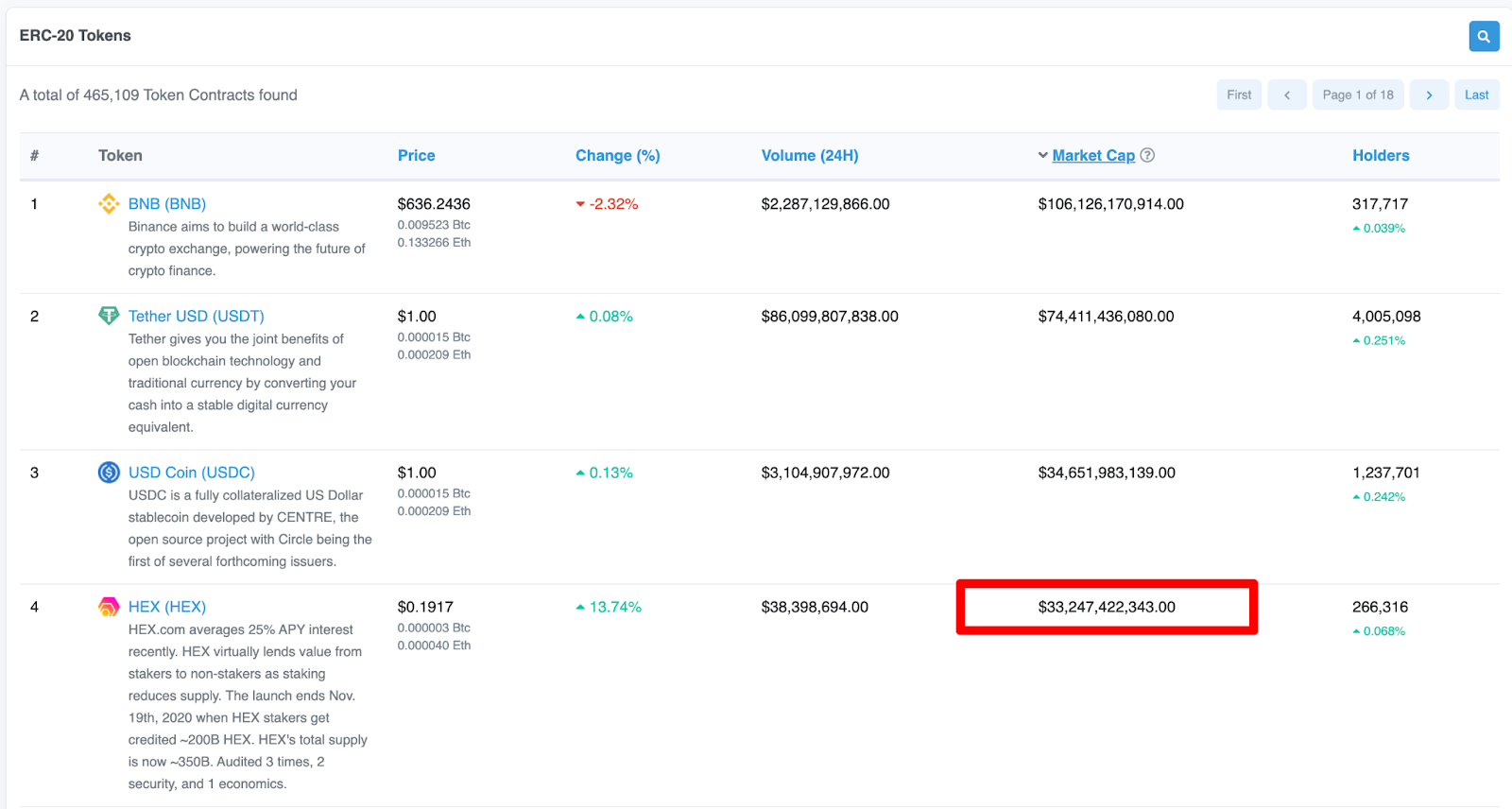

Every once in a while, we screw up and a no-name asset pops above ETH or BTC on our front page.

Here’s an example…

@ClayCollins @NomicsFinance yall fukn up bro. pic.twitter.com/e7gHpVlYNZ

— Hex_julio (@Hex_Julio) November 8, 2021

Often, these anomalies (visualized in the image above) appear when:

- Founders, developers, and project wallets control 90%+ of the supply, and …

- Only a small fraction of the total supply (i.e. 10% or less) is used to price the remaining 90%+ of assets

Here’s how to get a #1 market cap asset in less than an hour…

- Step 1: Mint 100 Trillion BEP-20 Tokens on Binance Smartchain.

- Step 2: Give all but 100 to yourself.

- Step 3: Put the remaining 100 on PancakeSwap against 0.1BNB and then buy a token.

Done.

You now have a higher market cap asset than bitcoin. Which is why, as Richard Heart says, “Market cap is a silly made up number and always has been.”

Indeed, it’s my understanding that the irrelevance of market cap is a core part of the HEX narrative. That is, the only thing that matters as an investor is price appreciation and having enough liquidity to take profit (when needed) without killing the price. (Congrats to HEX holders, BTW, on being up 2,009.71% in the last year).

HEX — with a two-year track record and 70K stakers — isn’t the same as the no-name coins that Nomics mistakenly ranks above ETH and BTC occasionally. But many projects do engage with the market cap manipulation tactics numbered above. And if we didn’t omit project & founder controlled tokens, you’d see at least 10 scams, every day, ranking above Bitcoin (and HEX for that matter).

Introducing the SquareCircle Case Study

Recently, we heard from a project called “SquareCircle Coin” (the name has been changed for this case study).

Here’s some data on SquareCircle Coin:

- Their top wallet had 99.999899% of the assets

- Their last price on Pancakeswap was $0.022362

- If you consider only the pancakeswap assets as the circulating supply (so, just dex liquidity) their market cap is ~$3

- If you take their claim at face value, their market cap is $582,000,000,000, which is a touch more than ETH

My point is this…

… if Nomics counted 100% of issued supply of all tokens as “circulating” then every day there would be several assets ranking above Bitcoin (and HEX for that matter) and nobody would believe us.

This is why, when projects come to us, we send them the following…

1. Please explain the top 10 holders shown in the block explorer link you submitted.

2. Please submit all addresses that are held by the team, project, developers, marketing, advisors, or anyone else involved in the project.

3. Please submit all addresses that are used to burn or deploy tokens

4. Please submit all addresses that are otherwise non-circulating

For each item above if there are no addresses that fit this category, submit “None.”

(Nomics Survey For Crypto Projects Issuing Assets on Smart Contract Platforms)

For tokens issued on smart contract platforms (e.g. ERC-20 or BEP-20 tokens) we do not count assets as circulating if they are in:

- Wallets held by the project owner and team members

- Wallets designated for development, marketing, airdrops, giveaways

- Burn wallets

- Deployers

- Any other wallet that is locked or non-circulating for another reason

- Wallets hard-coded into the asset smart contract to receive token distributions

For Proof-of-Work assets with no known pre-mine, we count all issued tokens as circulating unless we have specific/concrete datapoints to suggest that assets should be removed from circulation (this is the hard part).

… now let’s proceed with an FAQ

Q: What’s Happening?

A: We’re changing the Hex circulating supply, which will affect Hex’s market cap.

Q: Why Are You Showing Hex’s Market Cap on the Front Page of Nomics While CoinMarketCap and CoinGecko are Not?

The market cap rank of Hex is obviously not #201 (or whatever CoinMarketCap has it at right now).

I think almost everyone — including Hex haters — would agree it’s higher than this.

CoinGecko is dodging the issue by not assigning a market cap at all. I must admit that because HEX OA ownership is difficult to understand, I’ve also wanted to avoid having to make a determination about HEX supply.

Q: Isn’t Market Cap Stupid?

A: Yes (see Richard Heart quote at the top). We agree it’s not the best metric.

But it’s what people want, and it’s foolish to try and fight this.

In a few instances, companies have tried to rank cryptoassets by other metrics, and the market has rejected such approaches.

We believe that the market will eventually evolve past prioritizing market cap, but we’re not there yet.

Q: Isn’t Market Cap A Simple Multiplication of Supply x Price?

“Fully diluted” (which really means fully inflated) market cap is total supply x price. But plain-ol’ market cap is generally taken to be price x circulating supply.

But there are a lot of decisions to be made here, like “how much volume is needed to establish a price (does $10 of trading activity count)?”

At the very top of this article, we explain why market caps determined by simple math — and no value judgements — result in rankings that people don’t trust.

Which is why we approach crypto data from largely unregulated exchanges like a spam problem. Indeed, it is our understanding that most people view market capitalization rankings as a proxy for the relevance/impact of crypto assets (and exchange volume as a proxy for relevance/impact of crypto exchanges). And in a manner similar to Google/SEO spam, many projects try and hack these rankings.

- Exchanges try and hack their ranking by faking volume

- Crypto projects try and hack their market cap by issuing untradable supply (that increases market cap via the cap = price * supply equation) and manipulating price

Which is why we modulate exchange rankings and exchange markets with our impact score, and we take action on project ownership outliers (i.e. situations when the vast majority of an asset is untradeable and unavailable to count toward price discovery, yet counting towards market cap).

Q: Why Are You Changing The Hex Circulating Supply?

A:

Roughly 90% of HEX is owned by the OA and has never moved.

Of the user owned HEX, roughly 70% is staked.

We are listed on zero major exchanges.

Most trading happens on dexes like uniswap and 1inch.

Smart people don’t trade #HEX they stake it.

— HEXtronaut (@HEXtronaut) September 22, 2021

This tweet above is directionally correct.

In fact, according to the most thorough reporting we can find on HEX supply (i.e. the Hex Audit Telegram group and this spreadsheet), 11.81% of HEX is owned by users.

According to the methodology that we apply to all assets issued on Smart Contract platforms (see the questions mentioned in the intro), we have decided to not count OA Ownership as circulating.

Q: The OA Tokens *Can* Be Moved And Staked… Why Don’t You Consider Them Circulating?

The OA tokens have never been sold (and they do not behave like assets in circulation). Moreover, they are excluded by our methodology.

For tokens issued on smart contract platforms (i.e. ERC-20 or BEP-20 tokens) we do not count assets as circulating if they are in

- Wallets held by the project owner and team members

- Wallets designated for development, marketing, airdrops, giveaways

- Burn wallets

- Deployers

- Any other wallet that is locked or non-circulating for another reason

- Wallets hard-coded into the asset smartcontract to receive token distributions

We agree that these assets *can* be sold… but they never have been, and according to our methodology (which we apply across the board), as long as they are project controlled, we consider them to not be in circulation.

Q: So Circulating Supply Is Subjective?

Yes. Absolutely.

There is no commonly accepted on-chain standard for deriving circulating. Even Etherscan (which is seen as impartial) has HEX’s market cap below USDC.

When it comes to supply, there are certainly judgement calls to make. For example…

- If a project issues 100 tokens, and keeps 90 of them within it’s treasury, and distributes the other 10, should spot price of the 10 assets be used to price the remaining tokens?

- Should founder held tokens be considered circulating?

- Should project-held tokens be considered circulating?

- Should assets sent to a burn address be considered circulating?

- Should POW tokens acquired during a pre-mine be considered circulating?

- Should lost cryptoassets, or cryptoassets belonging to deceased individuals be circulating?

- Should time-locked liquidity be considered circulating?

- If an asset hasn’t moved in 10 years, is it circulating?

As you can see, it can be difficult (if not impossible) to arrive at an on-chain way to consistently determine what’s circulating and what isn’t.

According to our methodology, HEX’s OA tokens will not be counted as circulating. At the time of writing, these tokens account for 88.19% of issued supply.

Q: What Is the HEX OA?

The HEX OA, or “Originating Address,” is an address named by the HEX token contract as the receiver of HEX tokens based on certain contract interactions, such as penalties from cancelled stakes. Additionally, we consider addresses whose sole activity has been to receive tokens from the OA to also be part of the OA network. For more information see the HEX Audit Telegram and spreadsheet.

Q: If Tim Cook Is Awarded Shares by Apple – They Are Added to Circulating Supply. They Are No Longer in Control of the Company. By Nomics Making a Differentiation and Combining Founders + Company/Project Tokens, You May Be Removing Transparency As It Doesn’t Help A User Understand If The Owners Can Dump

Generally speaking, by the time a company goes public (at least in the United States), you don’t see founders with controlling or majority ownership of a company.

For example…

- Jeff Bezos owns about 10% of Amazon

- Zuck owns about 14% of FB

In crypto, you can see founders owning 80%, 90%, or more. And behaving similarly to how companies behave with stock it controls.

There are enough instances where founder tokens are more qualitatively similar to project tokens — than they are similar to founder shares of a public company — to make excluding them a necessary step to cleaning up the top market cap list.

Q: This All Sounds Very Imprecise, Error-Prone, and Subjective

It absolutely is. Yes. Very imperfect and with flaws.

Q: Are You Saying That You’ve Been Incorrectly Inflating the HEX Market Cap Prior to Now?

We are saying that we have not been internally consistent. We have not applied the same standards to HEX’s circulating supply as we’ve applied to other ERC-20 and BEP-20 tokens, and now we’re taking steps to adjust this.

There’s a lot to understand about HEX ownership.

We didn’t understand HEX very well before and therefore counted almost all issued HEX tokens as circulating, which isn’t consistent with how we treat other assets issued on smart contract platforms.

Q: When Adding Circulating Supply to Nomics, You Require Projects to Disclose Project Addresses, Address of Owners, Burns Wallets, Deployers, Other Wallets with Non-Circulating Assets, and Wallets Hard-Coded Into the Smart Contract to Receive Distribution. What Happens If The Project Doesn’t Disclose This Information?

If a project is small (i.e. not top 50) and assets were issued by smart-contract creator that doesn’t disclose ownership publicly or respond to our questions, they generally do not receive a circulating supply value on Nomics.

For larger projects — where assets are issued by a smart-contract creator who does not answer our questions — we make our own judgements, which err on the conservative side (i.e. on the side of lower circulating supply).

With HEX, we’ve been unable to have a conversation with the anonymous owner of the OA, so we’ve leaned on the HEX audit and our own investigations, which have come to the same conclusions as the HEX audit.

Q: If the OA Had Different Figures and Were Willing to Engage With You to Update the Circulating Supply Number, Would You Engage With Them?

100%. Yes. Absolutely. We understand that they want to stay anonymous. Perhaps they can email support@nomics.com with a protonmail address or something similar? We’d love to have a dialogue with them.

Q: What About Satoshi’s Coins? What About Lost Bitcoins? What About ETH Owned by Vitalik?

This is a great point.

We’re more likely to take action…

- When an asset enters the top 10 (but especially the top 5)

- When there is a founder/project ownership outlier (i.e. when we believe founder/project ownership is over 50%)

- When a project is newer and assets were programmed into existence by smart contracts (i.e. where we see most of the rug pulls & market manipulation shenanigans happening)

- When a small set of addresses have the ability to drain all liquidity multiple times over (the biggest reason we dig in to a circulating supply claim is when a few top addresses are unexplained and hold more assets than exchanges — and liquidity pools do — because this generally means one person could rugpull the whole thing).

In other words, because this is a time-intensive, subjective, and manual process (with automated monitoring), we only have the bandwidth for high levels of scrutiny for high market cap assets that are outliers with regards to founder/project ownership.

Q: If the OA Owned 5% or 10% Would You Be Making This Move?

There’s a very good chance that with only 5% or 10% (or even 25%) OA ownership, we might not notice.

Q: Why Are You So Focused on HEX?

Prior to this adjustment, we ranked HEX at #3 (a higher — or equal — rank than any other major market cap sites for this asset).

A high percentage of support questions we get (including from HEXicans) basically ask “why does CoinMarketCap and/or CoinGecko say X While Nomics Says Y.”

So we’ve been asking questions about HEX … because we are constantly asked about it. And we needed information necessary to defend our position or reconsider it.

Essentially, the effort to intelligently respond to the inquirenes we received prompted us to ask questions about HEX.

Q: So If You Get A Lot Of Questions About An Asset, You Examine It Closer?

Q: What About Project X? I Believe Ownership There is Also Centralized But You’re Not Taking Action? Why Not?

Probably because we don’t know about it. Please send a support ticket to support@nomics.com and we’ll do our best.

Conclusion

I wish there were a one-sized-fits all impartial (and spam-proof) methodology for market cap that wasn’t subject to manipulation. But as far as we know, that doesn’t exist right now.

I believe that someday Nomics.com, and the industry as a whole, will move towards ranking by proprietary “influence scores” that factor datapoints from a variety of sources (i.e. social media mentions, website traffic, locked liquidity, on-chain activity) to determine the importance of a project … much like Google rankings.

If you have questions, comments, or criticisms, I invite you to leave them in the comments section below. Please be patient while we attempt to answer your questions (give me 24 business hours per question). We acknowledge upfront that you might have challenging questions that we cannot answer; these questions/comments will push us and the industry to evolve.

—Clay Collins (CEO of Nomics)